How a FICO Score is Calculated

A FICO score is pretty easy to calculate...the equation is simple, avaliable, and only made up of 5 pieces. Raising your FICO score can be easy...most of the time it is...how quickly it happens is a different story.

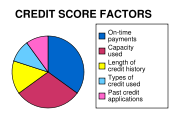

Your FICO score is made up of the following:

Quote from Wikipedia:

"35% punctuality of payment in the past (only includes payments later than 30 days past due)

"35% punctuality of payment in the past (only includes payments later than 30 days past due)

30% the amount of debt, expressed as the ratio of current revolving debt (credit card balances, etc.) to total available revolving credit (credit limits)

15% length of credit history

10% types of credit used (installment, revolving, consumer finance)

10% recent search for credit and/or amount of credit obtained recently "

1) Your first goal for raising your FICO score: PAY YOUR DEBT ONTIME. Most banks now provide you with the ability to access your account online. There are also a number of free programs that will send out your bill payments for you. If your bank does NOT provide this... switch your bank. If you have the money to pay your bills, there is absolutly NO EXCUSE for making a late payment. Set it up to be paid electronically...check it once a month to make sure your payments have been and are scheduled to go through...and forget about it. Paying your bills on time is the easiest way to improve your score...and if you aren't paying ontime...it won't really matter what you do...your score will go down.

2) The percentage of your credit used. Basically, if you have a credit card with a $5,000 limit and a balance of $4,000...your credit score will go down...the quickest way to improve your score...call your bank and ask for a credit limit increase. Most banks will immediatly approve your request for one simple reason. They want you to charge your cards up and pay them interest...Ideally, you will charge up your cards so much that you will pay and pay and pay...until you have nothing...and must declare bankrupcy (some banks aren't so evil...most are) If you get an increase to say...$10,000...you will only have 40% of your card limit taken as opposed to 80%. This will start to improve your score immediatly. After that...agressivly pay down credit cards with the highest percentage of avaliable credit used...your score will improve.

3) Credit history. Not much you can do there. Keep paying bills on time and don't charge up new debt and the history will take care of itself.

4) Credit used...Keep your credit to credit cards, small personal loans, and mortgages and avoid the payday loans.

5) Recent credit. Don't apply for a dozen credit cards at once. Don't apply for a new mortgage each month...don't buy a new car each month. Just be smart about the type of credit you take on.

So. Pay on time, pay it down, wait, don't get new debt, don't apply for more credit than you need.

Follow those lessons and your FICO score will improve.

Until next time,

Thor

Helpful Links:

http://en.wikipedia.org/wiki/FICO

Your FICO score is made up of the following:

Quote from Wikipedia:

"35% punctuality of payment in the past (only includes payments later than 30 days past due)

"35% punctuality of payment in the past (only includes payments later than 30 days past due)30% the amount of debt, expressed as the ratio of current revolving debt (credit card balances, etc.) to total available revolving credit (credit limits)

15% length of credit history

10% types of credit used (installment, revolving, consumer finance)

10% recent search for credit and/or amount of credit obtained recently "

1) Your first goal for raising your FICO score: PAY YOUR DEBT ONTIME. Most banks now provide you with the ability to access your account online. There are also a number of free programs that will send out your bill payments for you. If your bank does NOT provide this... switch your bank. If you have the money to pay your bills, there is absolutly NO EXCUSE for making a late payment. Set it up to be paid electronically...check it once a month to make sure your payments have been and are scheduled to go through...and forget about it. Paying your bills on time is the easiest way to improve your score...and if you aren't paying ontime...it won't really matter what you do...your score will go down.

2) The percentage of your credit used. Basically, if you have a credit card with a $5,000 limit and a balance of $4,000...your credit score will go down...the quickest way to improve your score...call your bank and ask for a credit limit increase. Most banks will immediatly approve your request for one simple reason. They want you to charge your cards up and pay them interest...Ideally, you will charge up your cards so much that you will pay and pay and pay...until you have nothing...and must declare bankrupcy (some banks aren't so evil...most are) If you get an increase to say...$10,000...you will only have 40% of your card limit taken as opposed to 80%. This will start to improve your score immediatly. After that...agressivly pay down credit cards with the highest percentage of avaliable credit used...your score will improve.

3) Credit history. Not much you can do there. Keep paying bills on time and don't charge up new debt and the history will take care of itself.

4) Credit used...Keep your credit to credit cards, small personal loans, and mortgages and avoid the payday loans.

5) Recent credit. Don't apply for a dozen credit cards at once. Don't apply for a new mortgage each month...don't buy a new car each month. Just be smart about the type of credit you take on.

So. Pay on time, pay it down, wait, don't get new debt, don't apply for more credit than you need.

Follow those lessons and your FICO score will improve.

Until next time,

Thor

Helpful Links:

http://en.wikipedia.org/wiki/FICO

posted by Thor @ 11:02 AM

![]()

0 Comments:

Post a Comment

<< Home